комментарии Тимофей Мартынов на форуме

-

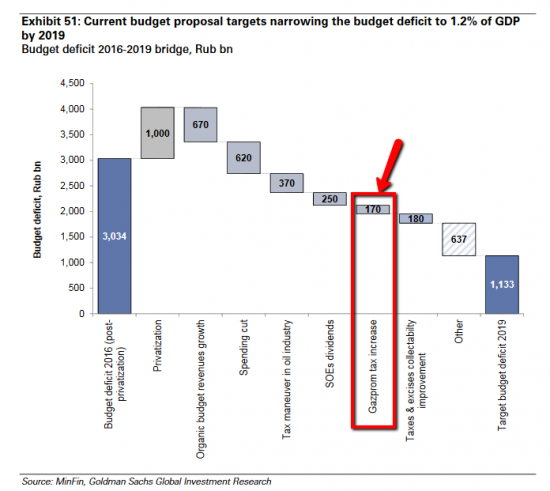

А кто что слышал про повышение налогов для Газпрома?

А кто что слышал про повышение налогов для Газпрома?

Голдман Сакс пишет, что это заложено в проект бюджета 2016-2019 годы в размере 170 млрд рублей

- Голдман позитивно смотрит на Аэрофлот:

Russians switch to domestic travel. As international trips became less affordable, as a result of ruble devaluation, Russian consumers revised their vacation plans to visit domestic tourist locations. In response, local carriers have redirected fleet capacity to domestic destinations. In 2016, the ytd share of domestic air traffic has grown to 57%, from 41% in 2014.

The main beneficiary of domestic air traffic growth is Aeroflot, which despite recent outperformance (up 64% vs. the MSCI EEMEA over the last three months), remains an attractive Buy (Rub131.7), in our view, owing to the benefits of market share gain (47% in 2016 vs. 37% in 2015), high dividends (8% yield) and supportive secular trends for LCC and transit market developments in Russia.  И ВТБ Капитал и Голдман Сакс среди потребительских компаний выделяют X5 Retail Group. Вот что пишет Голдман:

И ВТБ Капитал и Голдман Сакс среди потребительских компаний выделяют X5 Retail Group. Вот что пишет Голдман:We maintain our positive view on X5 as, in our view, its shares still fail to reflect:

(1) management’s plans to double the size of the business by 2020 (we are 11% ahead of Bloomberg consensus on 2017-19E sales) and a turnaround in supermarkets;

(2) scope to surprise on margin expansion (consensus expects EBITDA margin to decline in 2017-19E from the 2016 level);

(3) solid FCF; we forecast an inflection to positive flows from 2018, allowing deleveraging or trading of working capital for better supplier terms; and

(4) a supportive valuation (7.2x 2017E EV/EBITDA vs. 10.7x/9.1x for MGNT/CEEMEA peers). Многие аналитики выделяют именно Лукойл среди всех нефтяных компаний на 2017 год… Голдман Сакс не исключение:

Многие аналитики выделяют именно Лукойл среди всех нефтяных компаний на 2017 год… Голдман Сакс не исключение:Lukoil is our top pick in the Russian oil and gas space owing to:

(1) an attractive dividend outlook, fully covered by FCF (c.6%/7% 2016/17E dividend yield);

(2) a production turnaround post new field launches (we expect pr oduction growth of 3.7% yoy in 2017 vs. -2.6% yoy in 2016E);

(3) an expansion in pr ofitability and FCF growth on the back of an improvement in production dynamics (FCF yield of 13%/14% in 2017/18E) and a capex reduction. Голдман Сакс верит в выдающийся рост финпоказателей Яндекса в 2016 году и ставит эту бумагу как одну из лучших идей на 2017 год:

Голдман Сакс верит в выдающийся рост финпоказателей Яндекса в 2016 году и ставит эту бумагу как одну из лучших идей на 2017 год:We forecast a 27% EPS CAGR through 2017-20 on the back of: (1) a 16% revenue CAGR driven by further shifts in marketing budgets to online, navigation of the competitive pressure on mobile, and growth potential in other verticals (taxi, ecommerce and classifieds), which should contribute 40% to incremental 2017-20E revenues; and (2) EBITDA margin expansion to 38% in 2020E from 35% in 2016E, driven by operating leverage and improving monetization in verticals. The stock trades at 19x 2018E P/E, below global peers on a growth-adjusted ba sis, supporting our positive view.

Яндекс конечно еще однозначно будет расти...

Но честно говоря, при текущем P/E=50 покупать Яндекс кажется немного рискованно Ур Урычь, ух ничоси, ты где такую схему надыбал?

Ур Урычь, ух ничоси, ты где такую схему надыбал?

Добавил вашу схему в статью FCF нашего словаря Олеся Ветер, да, спасибо и за эту информацию

Олеся Ветер, да, спасибо и за эту информацию

это очень интересно

я кстати не думал что так бывает

то есть получается, что есть вероятность того, что оставшиеся акционеры проголосуют против?

молодец, следишь внимательно за всем:)- Олеся Ветер, спасибо!

короче мировой тренд

я так полагаю, что есть надежда на то, что Мегафон таким образом сможет оттяпать долю конкурентов если сумеет наладить эффективное взаимодействие с базой вконтактика Олеся Ветер, ну расскажи хотя бы, кто там продает эти акции мейла?

Сам Усманов или кто то еще?

ВТБ Капитал пишет, что на 2017 год ГМК — это наименее привлекательная бумага в секторе.

ВТБ Капитал пишет, что на 2017 год ГМК — это наименее привлекательная бумага в секторе.

ГМК торгуется на уровне EV/EBITDA=8 (2017), что в 2 раза больше аналогичного показателя Алросы- ВТБ-Капитал верит в Алросу:

ALRS’s stock is trading at a non-demanding below 4x EV/EBITDA for 2017F, and we expect it to generate 50% FCFE yield and pay a 30% dividend yield in the next three years. As we expect the diamond market to perform strongly in 2017, we believe the stock could well re-rate.

- aps, тут конечно вопрос веры. И если веришь в 50%, мне кажется в первую очередь надо тарить газпром

- aps, статус закона не помешал следующим госкомпаниям выплатить дивы ниже 50% МСФО:

Роснефть — 35%

Газпром — 24%

Транснефть — 9%

ИнтерРАО — 8%

Чтобы купить акции, выберите надежного брокера: